Value investing in India, applying principles of Buffett, Phil Fischer and other great investors. An attempt to discover undervalued stocks that can generate above average returns combining fundamental and technical analysis

Augustine’s feeling of fragmentation has its modern corollary in the way many contemporary young people are plagued by a frantic fear of missing out. The world has provided them with a superabundance of neat things to do. Naturally, they hunger to seize every opportunity and taste every experience. They want to grab all the goodies in front of them. They want to say yes to every product in the grocery store. They are terrified of missing out on anything that looks exciting. But by not renouncing any of them they spread themselves thin. What’s worse, they turn themselves into goodie seekers, greedy for every experience and exclusively focused on self. If you live in this way, you turn into a shrewd tactician, making a series of cautious semicommitments without really surrendering to some larger purpose. You lose the ability to say a hundred noes for the sake of one overwhelming and fulfilling yes.

Action orientation

What sort of mysterious creature is a human being, Augustine mused, who can’t carry out his own will, who knows his long-term interest but pursues short-term pleasure, who does so much to screw up his own life? This led to the conclusion that people are a problem to themselves. We should regard ourselves with distrust: “I greatly fear my hidden parts,”13 he wrote.

Small and Petty Corruptions

Oblique orientation

And so it is with tranquillity. If you set out trying to achieve inner peace and a sense of holiness, you won’t get it. That happens only obliquely, when your attention is a focused on something external. That happens only as a byproduct of a state of self-forgetfulness, when your energies are focused on something large.

The people we think are wise have, to some degree, overcome the biases and overconfident tendencies that are infused in our nature. In its most complete meaning, intellectual humility is accurate self-awareness from a distance. It is moving over the course of one’s life from the adolescent’s close-up view of yourself, in which you fill the whole canvas, to a landscape view in which you see, from a wider perspective, your strengths and weaknesses, your connections and dependencies, and the role you play in a larger story.

People who are humble about their own nature are moral realists. Moral realists are aware that we are all built from “crooked timber”—from Immanuel Kant’s famous line, “Out of the crooked timber of humanity, no straight thing was ever made.” People in this “crooked-timber” school of humanity have an acute awareness of their own flaws and believe that character is built in the struggle against their own weaknesses. As Thomas Merton wrote, “Souls are like athletes that need opponents worthy of them, if they are to be tried and extended and pushed to the full use of their powers.”12

Investors considering increasing portfolio risk should first consider asset allocation breakevens

About this time in a market cycle, after several years of strong stock market returns, there is a tendency for investors to become more tolerant of risk. One may find his or herself questioning the reasoning behind their current asset allocation and strongly considering adding more stocks and other "risk" assets to their portfolio.

Instead of writing about how to select an appropriate asset allocation, we want to bring to light a few important points that often go overlooked whenchangingan asset allocation, specifically when adding more risk to a portfolio.

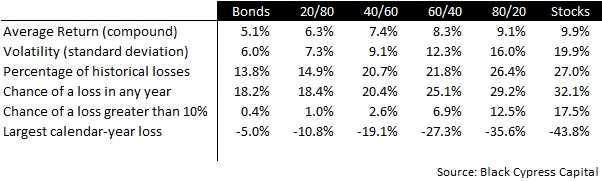

The table above contains the historical results of large U.S. stocks, U.S. bonds, and portfolios containing varying percentages of each from 1926 to 2014.

A few things should stand out. An all-stock portfolio generated the highest return, compounding capital at nearly 10% per year. This higher return came with much greater volatility: stocks experienced declines in greater frequency and in far greater severity than bonds.

Although stocks handily outperformed bonds over the entire 88 year history, there were periods where stocks underperformed for many years. Investments made in stocks during the late 1920s, mid 1960s, and late 1990s failed to beat bonds for stretches of ten or more years. About 20% of the time since 1926, stocks have underperformed bonds for 5-year stretches. So despite stocks' higheraveragereturns, the benefits from adding exposure have at times required lengthy time horizons to pay off. How then, should an investor approach raising their allocation to risk?

Asset Allocation

Above are the expected returns to different asset allocations assuming future returns that are consistent with historical returns. It is not our forecast of future asset allocation returns (we think returns will be lower). But for the sake of this discussion, starting with average returns removes any potential bias.

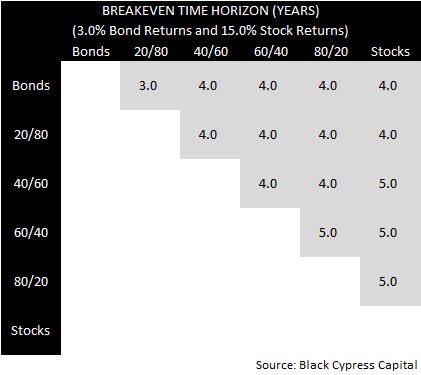

Let's start with an asset allocation of 60% stocks and 40% bonds. Assuming annual stock returns of 10.0% and bond returns of 5.0% (returns consistent with history), a 60/40 portfolio has an average expected return of about 8.0% per year. What if we wanted to increase the portfolio's exposure to stocks to 80%? An 80/20 portfolio would have an average annual expected return of 9.0%.

Should an investor make the switch to gain the extra 1.0% per year? Only if they have at least a decade to invest.

It might surprise you, but a passive* investor needs a time horizon of at least 10 years to have a high likelihood of outperforming their 60/40 portfolio when moving to an 80/20 portfolio. Why? Because stocks fall precipitously once or twice a decade.

Recessions and bear markets–both of which have historically occurred once or twice a decade–wipe out many years of the excess returns that are hoped to accompany the more aggressive asset allocations. During recession-driven bear markets, stocks have on average fallen about 30% and bonds have risen about 5%. In a typical recession, a 60/40 portfolio would be down about 16.0%, while an 80/20 portfolio would be down approximately 23.0%. Because losses have a magnified impact, raising risk in an asset allocation requires fairly long time horizons to ensure success (to overcome a future bear market setback). Here's the math.

If a $100,000 60/40 portfolio compounds at 8.0% per year for 9 years it will have risen to just shy of $200,000. An 80/20 portfolio will have risen to $217,000 (9.0% per year). If a typical bear market then immediately began, the 80/20 portfolio would decline to $167,000 (down 23%) while the 60/40 portfolio would fall to $168,000 (down 16%). Under these return assumptions, an investor in an 80/20 portfolio will have less money during a typical bear market than a 60/40 investor, should the decline occur any time before the 10th year.

The grid below contains the number of years necessary to ensure that a shift up the risk spectrum is rewarded if future returns are the same as historical returns.

Asset Allocation

What if we think future returns are going to be different than historical returns? Recommended time horizons change.

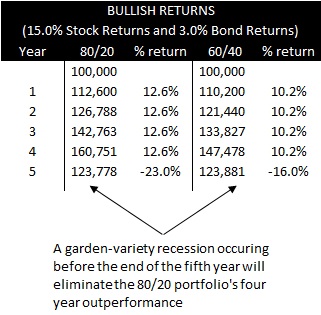

Stocks have risen over 21.0% per year since the bottom in 2009. Bonds are up a mid-single-digit percentage. What if the strong returns continue? What are breakevens if stocks return 15.0% per year and bonds 3.0% per year?

Under this bullish forecast, an investor still needs an investment horizon of five years before it makes sense to shift from a 60/40 portfolio to an 80/20 portfolio. If a bear market occurs any time before five full years of 15.0% stock returns and 3.0% bond returns, it would have been better to maintain the 60/40 portfolio.

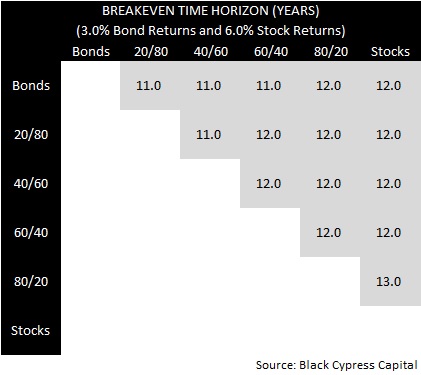

What if future returns are instead below historical averages? If returns over the next decade average 6.0% for stocks and 3.0% for bonds, then an investor's required time horizon stretches beyond a decade.

Asset Allocation

In the discussion above, we assumed a perfectly passive investor, one that selects an asset allocation, rebalances once per year, and makes no attempt to change their allocation to manage risk or to increase returns. Why does it make sense to approach this discussion with a passive investor in mind (when we are active investors)? For a couple of reasons.

While an active investor may attempt to manage risk successfully, their efforts may fail. By assuming no active skill and therefore average market returns, probable outcomes are evident and should therefore come with less surprise in the event that they do occur.

More important, by assuming passivity and average results, an investor is armed to make better active management decisions.

The breakeven time horizon to move a 60/40 portfolio to an all-stock portfolio (assuming historical returns) is 9 years. If there is reason to expect a recession-driven bear market well before the 9th year or that the stock market is priced for low future returns, then an investor is more likely to patiently wait for better opportunities, even if the stock market continues to rise.

With this in mind, we have a sound basis to mentally distance ourselves from the short-termism that drives markets. We can (and should):

– Aggressively buy stocks during bear markets and early in the market cycle

Once the stock market bottoms, it tends to rise 20%+ per year during the following two to three years.

Do not attempt to buy at some unknown and hoped for bottom, but buy consistently when there is "blood in the streets" (even if it is your own).

– Reduce the exposure to risk assets as a bull market ages and when future expected returns are low

The portfolio may very well underperform a more aggressive investment stance, but understand likely portfolio breakevens:

Stocks could rise 10.0% per year for 9 years and a 60/40 portfolio would still be larger than an all-stock portfolio in the middle of a garden-variety bear market.

– Hold cash when ideas are scarce.

– Think long-term (and win across a complete market cycle)

Do not try to outperform the stock market or the benchmark every year.

As the breakevens above show, it can be wise to manage risk even at the expense of short- to medium-term underperformance. If future returns are compressed, be patient and wait for better opportunities before increasing the exposure to risk assets.

The point is, breakeven analysis should lead to better decision-making because it encourages a more long-term oriented approach. And that long-term mindset should reduce emotional influences, even in the face of bear market turmoil or peak cycle euphoria.

Today, stock markets hover near all-time highs and appear priced to deliver below-average future returns. How low returns might be is up for some debate.

GMOpublishedits 7-year forecast last month and has large cap stocks returning 0.0% per year and small cap stocks losing 1.0% per year over the next 7 years. John Hussman of the Hussman Fundswrotetoday, "The most reliable measures we identify in market cycles across history are consistent with the expectation of near zero total returns in the S&P 500 Index over the coming decade, and the likelihood that the market will fall by half over the completion of the current cycle."

We are less bearish, expecting stock market returns over the next seven to ten years to be somewhere between 3.0% and 5.0% per year. The medium-term outlook, on the other hand, is still bright; we expect fairly solid stock market returns over the next two to three years as the U.S. and world economies continue to grow.

Our portfolio of 17 carefully chosen individual companies is priced to deliver double-digit annual returns.

It was too early to expect earnings to pick up. Whatever this government has done is left on implementation, but corporates have to follow through.

In an interview with ET Now, Kenneth Andrade, CIO, IDFC Mutual Fund, shares his views on markets. Excerpts:

ET Now: There is a section in the market which believes that the economic recovery in the first year of the current administration is slow. Is the criticism valid? Are you also disappointed, given the fact that earnings are yet to pick up?

Kenneth Andrade: I think it was too early to expect earnings to pick up. Whatever this government has done is left on implementation, but corporates have to follow through.

ET Now: So how will the second year of the government be different from the first?

Kenneth Andrade: As far as investment world is concerned, we look at the policy initiatives and we see how corporates follow them up. They do not have the balance sheet to follow it up. So, 2016 is not going to be very different from what you saw in 2015. And going into 2017, we need to see how demand actually picks up. So, capacities are there on the ground. They got created over the last 10 years. Demand and purchasing power have to come back, which will reflect in profitability. None of that is happening at this point in time.

ET Now: What lies ahead for the markets in the next year?

Kenneth Andrade: I do not think 10% is a retracement. It is just a normal correction that you get. As far as equities are concerned, our view has been that you would lose significant amount of capital but there will be a time element to it also. Market might just be around these levels, slightly lower or slightly higher but it will take time for it to actually evolve itself.

ET Now: And that some time could drag for the entire year?

Kenneth Andrade: It could be. We probably are in the minority as investment manager. We still think we are somewhere in the 90s in the previous investment cycle. A very large part of the population and investment community thinks we are in the early 2000s. We have to repair our balance sheet before we get going.

ET Now: Let us talk about companies which probably do not need that. If Janet Yellen's comments are anything to go by, the belief is that the US economy is stronger than what a lot of people believe, that would mean that the companies with exposure to the US markets could potentially do well? Are you playing the export theme because one, there is this commentary, two, their balance sheets are not under distress. Is that a good theme to play for the next 12 to 24 months?

Kenneth Andrade: If I look at our portfolio construction, we are still very domestically focussed and if you look at large international opportunities that are there, you probably get it for one or two sectors in the universe. One, you probably get it through IT, some little bit of ancillarisation of automobiles is there and then you get pharmaceuticals. Except for IT, which is largely cyclical, you add leverage into capex into the international environment.

That is the call that you need to take. But all said and done, valuations are also slightly trailing towards the higher side in this space. So, it is an equation of where you see larger growths coming in, how valuations stack up. We own IT but we are looking at companies that are doing things a little differently.

ET Now: So let us pull out your portfolio. Your fund is up 9% this year that is fantastic given that markets already have given a negative return. Your top holding is Page Industries, followed by SKS Micro Finance, Blue Dart, Vardhman Textiles, Ashok Leyland, Container Corporation. There is no similarity, what theme are you pursuing?

Kenneth Andrade: We always liked large companies. We like consolidators. We like businesses that come together and demonstrate pricing power and that is essentially what reflects in the portfolio.

ET Now: Are you not bothered about the PE multiple for a Blue Dart or for that matter a Page Industries? Blue Dart is trading at a PE multiple of 110 based on FY17 estimates?

Kenneth Andrade: We go through that very regularly. Our larger holdings would have another similarity with our large holdings that they will be trading at premium valuations to the entire portfolio. You take my top 10 bets and compare it with those of five-year back and they would be all between number 11 to number 20. We let the top 10 play itself out. They are good execution companies. They do not have too much financial risk. They do have a little bit of execution risk, but we are happy to play with that.

ET Now: Maruti and Idea are the only Nifty or rather bigger names over there. Why Idea, do you not believe that Rel Jio could be a threat whenever it comes about?

Kenneth Andrade: That is the only new competitor in that entire space, but if you look at it historically, that is an industry which has been consolidating quite fast. If you look at any business which consolidates fast, you will usually have the emergence of new player in the entire business, but my sense is that it will be very tough for Rel Jio to take it on.

ET Now: If you are indeed saying that the export-oriented themes are quite pricey, what do you find attractive now? what is it that could form a part of the 11 to 20 holdings right now? Which is the theme that you are playing?

Kenneth Andrade: There is no particular theme out there, but one thing we completely avoid is the infrastructure part of it all, whether it is liabilities or assets. We think that businesses require too much of capital to generate too little return. There is nothing there for the shareholders, there is everything there for the bankers out there. We are happy to sidestep that business.

ET Now: So banks are out?

Kenneth Andrade: You might just get a valuation part, but that might come. There is nothing structural in it. We might see a bank that will come into the portfolio over a period of time, but that will happen only if we find attractive valuations. On the asset side, it is a little easier to handhold these companies going forward, because they have no leverage. Banks for some reason are leveraged as disproportionately high at this point in time. They are grappling with way too many issues.

ET Now: Not every bank has an issue. PSU banks, by and large, have their own problems, but there are some good banks?

Kenneth Andrade: There might be one or two, which is why I do not rule it out. We have banks within the portfolio, but they are largely because of a strategy. So, there are a couple of banks which have demonstrated the ability to grow over the last decade and a half, but we do not think there are fair valuations at this point in time.

ET Now: What is the best way to bet on an economic revival? Because, if the economy comes back, banks and financials will do well. That is heart of your market also, 35%-36% benchmark weightages towards financials?

Kenneth Andrade: If I could answer that question a little differently, going by RBI data, 67% of all leverage in the banking system goes to corporate India and all of it goes to infrastructure. You cannot solve the problem by pumping more money into the same problem.

If you look at the entire business, you have an infrastructure business that is there. Equities have lost money, the banks are writing off NPAs. The government is not getting enough of money from the infrastructure assets and worse case consumers are paying more. So look at the value change, it does not make money for anyone.

ET Now: What is it that you are betting on on the asset side, which you think could revive as and when the economy comes back?

Kenneth Andrade: Consumer leverage will be back and that is more structural in nature than we have ever seen before or rather seeing right now. It is a long-term call that you have to take, but if banks have to deleverage or banks have to get into new spaces, that 67% loan book to industries is unsustainable. You have to break it down.

1. “Smart idea, grounded on exhaustive

research, followed by a big bet.”

“Hear a story, analyze and buy

aggressively if it feels right.”

A colleague of Robertson once said: “When he is convinced that he is

right, Julian bets the farm”

George Soros and Stanley Druckenmiller are similar. Big mispriced bets don’t

appear very often and when they do people like Julian Robertson bet big. This is

not what he has called a “gun slinging”approach, but rather a patient

approach which seeks bets with odds that are substantially in his favor.

Research and critical analysis are critical for Julian Robertson. Being patient, disciplined

and yet aggressive is a rare combination and Robertson has proven he has each of

these qualities.

2. “Hedge funds are the antithesis of baseball. In

baseball you can hit 40 home runs on a single-A-league team and never get paid a

thing. But in a hedge fund you get paid on your batting average. So you go to

the worst league you can find, where there’s the least competition. You can bat

400 playing for the Durham Bulls, but you will not make any real money. If you

play in the big leagues, even if your batting average isn’t terribly high, you

still make a lot of money.”

“It is easier to create the batting average in a lower league

rather than the major league because the pitching is not as good down there.

That is consistently true; it is easier for a hedge fund to go to areas where

there is less competition. For instance, we originally went into Korea well

before most people had invested in Korea. We invested a lot in Japan a long time

before it was really chic to get in there. One of the best ways to do well in

this business is to go to areas that have been unexploited by research

capability and work them for all you can.”

“I suppose if I were younger, I would be

investing in Africa.”

What Julian Robertson is saying is that there is profit for an investor

in going to where the competition is weak. Competing in markets that are less

well researched give an investor who does their research an advantage. Charlie

Munger was once asked who he was most thankful for in all his life. He answered

that he was as most thankful for his wife Nancy’s previous husband. When asked

why this was true he said: “Because he was a drunk. You need to make sure the

competition is weak.”

Warren Buffett makes the point that the way to beat Bobbie Fisher is to

play him at something other than chess. Buffett adds: “The

important thing is to keep playing, to play against weak opponents and to playfor big

stakes.” And “If you’ve been playing poker for half an hour and you still don’t

know who the patsy is, you’re the patsy.” Some investors try to

find a market or a part of a market where you aren’t the patsy if you want

to outperform an index.

3. “I believe that the best way to manage

money is to go long and short stocks. My theory is that if the 50 best stocks you can come up

with don’t outperform the 50 worst stocks you can come up with, you should be in

another business.”

The investing strategy being referred to here is a so-called

“long-short” approach in which long and short positions are taken in various

stocks to try to hedge exposure to the broader market which makes gains more

associated with solid stocking picking. This approach is actually involves an

attempt to hedge exposure to the market, unlike some hedge fund strategies that

involve no real hedging at all. When Julian Robertson started using this this

long-short approach it was less used and short bets especially were more likely

to be mispriced than they are today. Many of Julian Robertson’s so-called “Tiger

Cubs” continue to do long-short investing. A recent report claims that $687

billion is currently invested in long-short equity hedge funds.

4. “Avoid big losses. That’s the way to

really make money over the years.”

JulianRobertson believes that hedge fund

should make it a priority to “outperform the market in bad times.” That means adopting a strategy where the

hedge fund actually hedges. As previously noted, the long-short strategy helps

achieve that objective. Anotherway to avoid “big losses” is to buy an asset

at a substantial

discount to its private market value.When the right entry point is found in

terms of price, an investor can make

a mistake and still come out OK financially. This, of course, is a margin of

safety approach.

5. “For my shorts, I look for a bad

management team, and a wildly overvalued company in an industry that is

declining or misunderstood.”

When an investor shorts a company with a bad management team it is a

safer bet since a business with a good management team is far more likely to fix

problems. In other words, if a shorted business has a bad management team it is

insurance that the real business problem problem underlying the short will

continue. Julian Robertson is also saying that the overvaluation must be “wild”

rather than mild for him to be interested in a short, and that he likes shorts

in an industry in secular decline so the wind is at his back.

6. “There are not a whole lot of people

equipped to pull the trigger.”

“I’m normally the trigger-puller

here.”

The system used by Julian Robertson may decentralize the research and

analysis function but it concentrates the trigger pulling with him. The newsletter Hedge

Fund Letters writes: “Managers oversaw

different industries and made recommendations but Robertson had final say. The

firm made large bets where they had conviction and each manager commonly covered

less than ten long and shorts. Positions were continuously revisited and if

things changed there were no holds – positions were either added to or removed.”Someone can be a great analyst and

yet a lousy trigger puller.

Successful trigger pulling requires psychological control since most investing

mistakes are emotional rather than analytical.

7. “I’ve never been particularly

comfortable with gold as an investment. Once it’s discovered none of it is used

up, to the point where they take it out of cadavers’ mouths. It’s less a

supply/demand situation and more a psychological one – better a psychiatrist to

invest in gold than me.”

“Gold bugs, generally speaking, are some

of the craziest people on the face of the globe.”

“The second major category of investments involves assets that will

never produce anything, but that are purchased in the buyer’s hope that someone

else — who also knows that the assets will be forever unproductive — will pay

more for them in the future. Tulips, of all things, briefly became a favorite of

such buyers in the 17th century. This type of investment requires an expanding

pool of buyers, who, in turn, are enticed because they believe the buying pool

will expand still further. Owners are not inspired by what the asset itself can

produce — it will remain lifeless forever — but rather by the belief that others

will desire it even more avidly in the future. The major asset in this category

is gold, [favored by investors] who fear almost all other assets, especially

paper money (of whose value, as noted, they are right to be fearful). Gold,

however, has two significant shortcomings, being neither of much use nor

procreative. True, gold has some industrial and decorative utility, but the

demand for these purposes is both limited and incapable of soaking up new

production. Meanwhile, if you own one ounce of gold for an eternity, you will

still own one ounce at its end. What motivates most gold purchasers is their

belief that the ranks of the fearful will grow.”

To buy gold is to speculate based on your predictions about human

psychology. That is not investing, but rather speculation. A gold speculator is

engaged in a Keynesian Beauty contest: “It is not a case of choosing those

[faces] that, to the best of one’s judgment, are really the prettiest, nor even

those that average opinion genuinely thinks the prettiest. We have reached the

third degree where we devote our intelligences to anticipating what average

opinion expects the average opinion to be. And there are some, I believe, who

practice the fourth, fifth and higher degrees.” (Keynes, General Theory of

Employment, Interest and Money, 1936).

8. “When you manage money, it takes over

your whole life. It’s a 24-hour-a-day thing.”

This is a quote fromthe book Hedge Fund Masters on the Rewards, the Risk, and the

Reckoning byKatherine

Burton. Julian Robertson is not alone in this way since many financial and tech

billionaires only turn to things like philanthropy after a career change. This

is also a statement about how competitive and constantly changing the investing

world is. Only an academic like Bob Gordon who is not involved in the real world

can make a claim that the pace of innovation is slowing. The pace of innovation

is increasing and its impact is brutal. With regard to innovation and the level of competition in hedge funds,

Roberto Mignone, head of Bridger Management said once: “You’ve got a better

chance surviving as a crack dealer in Chicago than lasting four years in the

hedge fund business.”

9. “The hedge fund business is about

success breeding success.”

One of my favorite essays was written by Duncan Watts and is

entitled: Is

Justin Timberlake a Product of Cumulative Advantage? The concept of cumulative advantage is so important in understanding

outcomes in life and yet it is so poorly understood. The basic idea is that once

a person or business gains a small advantage over others, that advantage will

compound over time into an increasingly larger advantage. This is sometimes called “the rich get

richer and the poor get poorer” or “the Matthew effect” based on a biblical

reference. Merton used this cumulative advantage concept to explain advancement

in scientific careers, but it is far broader in it application. Cumulative

advantage operates as a general mechanism which increases inequality and

explains why wealth and incomes follow the power law described by Pareto. Part of what Robertson is saying is that the more money you

raise, the more money you can raise [repeat] the more talent you can attract,

the more talent you can attract [repeat].

10. ” I remember one time I got on the

cover of Business Week as “The World’s Greatest Money Manager.”

Everybody saw it and I was kind of impressed with it, too. Then three years

later the same author wrote the most scathing lies. It’s a rough racket. But I

think it’s a good thing in human narcissism to realize you go from highs and

lows based on your views from the press – really, it shouldn’t matter.”

Letting the views of the press on you impact your view of yourself or

what you do is folly. Criticism is hard to take for most anyone, but considering the source is

helpful in getting past that. The only thing that everyone likes is pizza. My uncle who recently passed away liked to say ‘Illegitimi non carborundum’ which is a mock-Latin aphorism

meaning: “Don’t let the bastards grind

you down.”This saying was popularized by US General Vinegar Joe Stillwell

during World War II, who is said to have borrowed it from the British army.

11. “[In March 2000] This approach isn’t

working and I don’t understand why. I’m 67 years old, who needs this? [In March

2000] There is no point in subjecting our investors to risk in a market which I

frankly do not understand. After thorough consideration, I have decided to

return all capital to our investors. I didn’t want my obituary to be ‘he died

getting a quote on the yen’.”

Sometimes the world changes so much that it is time to either take a

break or hang up your cleats – especially if you are already very rich. Some

people do this successfully. Others ride old methods to their financial doom.

Druckenmiller and others decided to mostly retire when they saw that their

methods were no longer working. In 1969, Warren Buffett wrote a letter to his

partners saying that he was “unable to find any bargains in the current market,”

and he began liquidating his portfolio. That situation of course changed and

Warren Buffett emerged with a new competitive weapon in the form of the

permanent capital of a corporation rather than the panicky capital of a

partnership.

12. “[At the age of six.] I still remember

the first time I ever heard of stocks. My parents went away on a trip, and a

great-aunt stayed with me. She showed me in the paper a company called United

Corp., which was traded on the Big Board and selling for about $1.25. And I

realized that I could even save up enough money to buy the shares. I watched it.

Sort of gradually stimulated my interest.”

If you want a child to be interested in investing it is wise to

introduce key ideas to them early in life in real form. No matter how small the stake, the

impact of real money at work in a market means the experience is meaningful and

memorable. Mary Buffett writes in her book that Warren Buffet believes that

whether a person will be successful in business is determined more by whether a

person had “a lemonade stand as a child than by where they went to college. An

early love of being in business equates later in life to being successful in

business.”

Below find an excerpt taken from an interview between Raoul Pal and Kyle Bass (a hedge fund manager based out of Texas.)

What resonates with me here is the need to find a way out of a world where we are pulled in a thousand different directions and find an internal quiet. In turn these quiet and intimate moments with ourselves enable us to excel.

Pal was asking about how Bass keeps balance in his life.

Kyle Bass: I’ve searched for that my whole life. I found it about six years ago. My favorite thing in the world is to do freediving and spearfishing. I know you live on an island. I could do that if I wasn’t running this firm, meaning as a lifestyle choice. I have a little Hemingway in me.

Raoul Pal: What is it about spearfishing and freediving that you like? I don’t spearfish. Freediving, I’ve had lessons in, and it’s a fascinating thing because it’s very internal.

Kyle: It’s internal. It’s a beautiful thing. It’s like when you think about the greatest battles in the world, they’ve always been civil wars, just like I think the greatest battles you and I fight are in our head. It’s between ourselves. The biggest battles that most people fight are with themselves.

When I was in college, I helped pay for college through … I had a diving and an academic scholarship. I was, primarily, a springboard diver. That was, I would say, 80 percent mental, 20 percent physical, even though it looks all physical. It’s you versus yourself. It’s you convincing yourself that you can do this, and do it as well or better than anyone else.

Freediving, very similar. It’s you knowing yourself. It’s you teaching yourself how to regulate your heart rate. It’s how to control your emotions. It’s made me better at controlling my emotions in the office.

Raoul: It’s kind of where I was going to get to this.

Kyle: The beautiful part of freediving for me and spearfishing is the day-to-day “grind” that we go through. My phone rings 24/7. I take that back. I turn my phone off at night, so there’s only a select few that can get through at night.

But during the day, I’m pulled in a thousand different directions. Regardless of how much I try to control my path through the day, things pop up. You have people everywhere pulling you 50 different ways.

The moment I go underwater in the ocean, it’s Zen-like for me. My phone can’t ring. No one can bother me. I’m typically there with people that I want to be there with, my team. I always dive with a team. Then it’s me versus myself. It literally is Zen-like, and I’ve gotten so much better at being calm that I go 8-10 hours a day.

Raoul: Wow. Because a lot of people do the similar thing with yoga, and actually, yoga and freediving have a lot in common.

Kyle: Do they?

Raoul: Yeah. Lots of the great freedivers now learn yoga to understand how to control their body and control their minds.

Kyle: I have a problem with yoga. My mind drifts. When I’m freediving, I’m focused. I’m focused on the potential threats, because I primarily do it all in the Bahamas, so we see sharks every day. I’m not that afraid of sharks. I respect them.

The difference, for me, between yoga and freediving is in yoga you’re sitting there, and you’re in a solitary moment, and you’re trying to focus on things mentally. But — I don’t know, I need the freediving aspect of it to be really centered. … That’s how I get centered.

Raoul: Yeah, you have a physical focus then, as well.

Kyle: Yeah. I’m always searching for the next great hogfish, or grouper, or lobster to eat that night. We eat what we shoot. It’s a beautiful, beautiful cycle that I go through, and I can do it for weeks on end.

Raoul: When did you take up freediving, and how did it change you in terms of how you work?

Kyle: It didn’t, initially. It was just something I’d always wanted to do. I found a young man on an island in the Bahamas. I asked around and said, “Who’s the best spearfisherman on the island?” Everybody said, “It’s Dave. It’s Dave. It’s Dave.”

This 17-year-old kid who had been bitten by sharks on his hand. He had been cut up on his foot by a propeller, and he’s just a great kid. Over the years, he’s become my boat captain. He’s now, I guess, 23 years old. We’ve been partners now for six years. Every moment, every chance I get for vacation, that’s where I go.

Raoul: As I said, you’ve actually noticed that whole process of learning that spill into your work, and it makes you calmer in how think about things?

Kyle: Yeah. You have to stay focused. If you trade on emotion, you lose every time. Every time. If you can divorce yourself of that, especially those real extreme and extremist, those emotions you feel, you have to go the other way. You have to

The single most common cause of cognitive-based errors was the tendency to stop considering other possible explanations after reaching a diagnosis.

When forming an opinion on a business or management team, it can be easy to ignore evidence or quit thinking when new information arrives, especially if the evidence contradicts the opinion one has already formed. And it can be easy to think that once an opinion is formed, the work is done and thus the effort to learn more to try and disprove that opinion stops.

When returns on capital are ordinary, an earn-more-by-putting-up-more record is no great managerial achievement. You can get the same result personally while operating from your rocking chair. Just quadruple the capital you commit to a savings account and you will quadruple your earnings. You would hardly expect hosannas for that particular accomplishment. Yet, retirement announcements regularly sing the praises of CEOs who have, say, quadrupled earnings of their widget company during their reign - with no one examining whether this gain was attributable simply to many years of retained earnings and the workings of compound interest.

If the widget company consistently earned a superior return on capital throughout the period, or if capital employed only doubled during the CEO’s reign, the praise for him may be well deserved. But if return on capital was lackluster and capital employed increased in pace with earnings, applause should be withheld. A savings account in which interest was reinvested would achieve the same year-by-year increase in earnings - and, at only 8% interest, would quadruple its annual earnings in 18 years.

The power of this simple math is often ignored by companies to the detriment of their shareholders. Many corporate compensation plans reward managers handsomely for earnings increases produced solely, or in large part, by retained earnings - i.e., earnings withheld from owners. For example, ten-year, fixed-price stock options are granted routinely, often by companies whose dividends are only a small percentage of earnings.

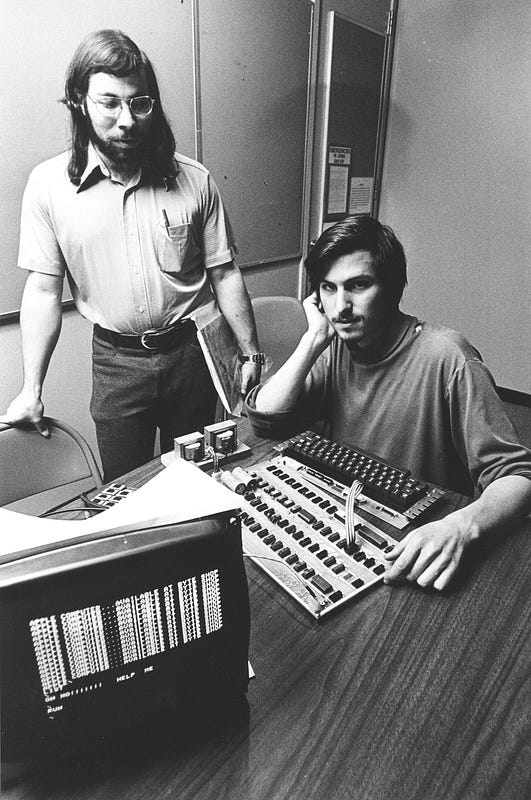

“You can’t really understand what is going on now without understanding what came before.”

Steve Jobs is explaining why, as a young man, he spent so much time with the Silicon Valley entrepreneurs a generation older, men like Robert Noyce, Andy Grove, and Regis McKenna.

It’s a beautiful Saturday morning in May, 2003, and I’m sitting next to Jobs on his living room sofa, interviewing him for a book I’m writing. I ask him to tell me more about why he wanted, as he put it, “to smell that second wonderful era of the valley, the semiconductor companies leading into the computer.” Why, I want to know, is it not enough to stand on the shoulders of giants? Why does he want to pick their brains?

“It’s like that Schopenhauer quote about the conjurer,” he says. When I look blank, he tells me to wait and then dashes upstairs. He comes down a minute later holding a book and reading aloud:

Steve Jobs and Robert Noyce. Courtesy Leslie Berlin.

He who lives to see two or three generations is like a man who sits some time in the conjurer’s booth at a fair, and witnesses the performance twice or thrice in succession. The tricks were meant to be seen only once, and when they are no longer a novelty and cease to deceive, their effect is gone.

History, Jobs understood, gave him a chance to see — and see through — the conjurer’s tricks before they happened to him, so he would know how to handle them.

Flash forward eleven years. It’s 2014, and I am going to see Robert W. Taylor. In 1966, Taylor convinced the Department of Defense to build the ARPANET that eventually formed the core of the Internet. He went on to run the famous Xerox PARC Computer Science Lab that developed the first modern personal computer. For a finishing touch, he led one of the teams at DEC behind the world’s first blazingly fast search engine — three years before Google was founded.

Visiting Taylor is like driving into a Silicon Valley time machine. You zip past the venture capital firms on Sand Hill Road, over the 280 freeway, and down a twisty two-lane street that is nearly impassable on weekends, thanks to the packs of lycra-clad cyclists on multi-thousand-dollar bikes raising their cardio thresholds along the steep climbs. A sharp turn and you enter what seems to be another world, wooded and cool, the coastal redwoods dense along the hills. Cell phone signals fade in and out in this part of Woodside, far above Buck’s Restaurant where power deals are negotiated over early-morning cups of coffee. GPS tries valiantly to ascertain a location — and then gives up.

When I get to Taylor’s home on a hill overlooking the Valley, he tells me about another visitor who recently took that drive, apparently driven by the same curiosity that Steve Jobs had: Mark Zuckerberg, along with some colleagues at the company he founded, Facebook.

“Zuckerberg must have heard about me in some historical sense,” Taylor recalls in his Texas drawl. “He wanted to see what I was all about, I guess.”

To invent the future, you must understand the past.

I am a historian, and my subject matter is Silicon Valley. So I’m not surprised that Jobs and Zuckerberg both understood that the Valley’s past matters today and that the lessons of history can take innovation further. When I talk to other founders and participants in the area, they also want to hear what happened before. Their questions usually boil down to two: Why did Silicon Valley happen in the first place, and why has it remained at the epicenter of the global tech economy for so long?

I think I can answer those questions.

First, a definition of terms. When I use the term “Silicon Valley,” I am referring quite specifically to the narrow stretch of the San Francisco Peninsula that is sandwiched between the bay to the east and the Coastal Range to the west. (Yes, Silicon Valley is a physical valley — there are hills on the far side of the bay.) Silicon Valley has traditionally comprised Santa Clara County and the southern tip of San Mateo County. In the past few years, parts of Alameda County and the city of San Francisco can also legitimately be considered satellites of Silicon Valley, or perhaps part of “Greater Silicon Valley.”

The name “Silicon Valley,” incidentally, was popularized in 1971 by a hard-drinking, story-chasing, gossip-mongering journalist named Don Hoefler, who wrote for a trade rag called Electronic News. Before, the region was called the “Valley of the Hearts Delight,” renowned for its apricot, plum, cherry and almond orchards.

“This was down-home farming, three generations of tranquility, beauty, health, and productivity based on family farms of small acreage but bountiful production,” reminisced Wallace Stegner, the famed Western writer. To see what the Valley looked like then, watch the first few minutes of this wonderful 1948 promotional video for the “Valley of the Heart’s Delight.”

Three historical forces — technical, cultural, and financial — created Silicon Valley.

Technology

On the technical side, in some sense the Valley got lucky. In 1955, one of the inventors of the transistor, William Shockley, moved back to Palo Alto, where he had spent some of his childhood. Shockley was also a brilliant physicist — he would share the Nobel Prize in 1956 — an outstanding teacher, and a terrible entrepreneur and boss. Because he was a brilliant scientist and inventor, Shockley was able to recruit some of the brightest young researchers in the country — Shockley called them “hot minds” — to come work for him 3,000 miles from the research-intensive businesses and laboratories that lined the Eastern Seaboard from Boston to Bell Labs in New Jersey. Because Shockley was an outstanding teacher, he got these young scientists, all but one of whom had never built transistors, to the point that they not only understood the tiny devices but began innovating in the field of semiconductor electronics on their own.

And because Shockley was a terrible boss — the sort of boss who posted salaries and subjected his employees to lie-detector tests — many who came to work for him could not wait to get away and work for someone else. That someone else, it turned out, would be themselves. The move by eight of Shockley’s employees to launch their own semiconductor operation called Fairchild Semiconductor in 1957 marked the first significant modern startup company in Silicon Valley. After Fairchild Semiconductor blew apart in the late-1960s, employees launched dozens of new companies (including Intel, National and AMD) that are collectively called the Fairchildren.

The Fairchild 8: Gordon Moore, Sheldon Roberts, Eugene Kleiner, Robert Noyce, Victor Grinich, Julius Blank, Jean Hoerni, and Jay Last. Photo courtesy Wayne Miller/Magnum Photos.

Equally important for the Valley’s future was the technology that Shockley taught his employees to build: the transistor. Nearly everything that we associate with the modern technology revolution and Silicon Valley can be traced back to the tiny, tiny transistor.

Think of the transistor as the grain of sand at the core of the Silicon Valley pearl. The next layer of the pearl appeared when people strung together transistors, along with other discrete electronic components like resistors and capacitors, to make an entire electronic circuit on a single slice of silicon. This new device was called a microchip. Then someone came up with a specialized microchip that could be programmed: the microprocessor. The first pocket calculators were built around these microprocessors. Then someone figured out that it was possible to combine a microprocessor with other components and a screen — that was a computer. People wrote code for those computers to serve as operating systems and software on top of those systems. At some point people began connecting these computers to each other: networking. Then people realized it should be possible to “virtualize” these computers and store their contents off-site in a “cloud,” and it was also possible to search across the information stored in multiple computers. Then the networked computer was shrunk — keeping the key components of screen, keyboard, and pointing device (today a finger) — to build tablets and palm-sized machines called smart phones. Then people began writing apps for those mobile devices … .

You get the picture. These changes all kept pace to the metronomic tick-tock of Moore’s Law.

The skills learned through building and commercializing one layer of the pearl underpinned and supported the development of the next layer or developments in related industries. Apple, for instance, is a company that people often speak of as sui generis, but Apple Computer’s early key employees had worked at Intel, Atari, or Hewlett-Packard. Apple’s venture capital backers had either backed Fairchild or Intel or worked there. The famous Macintosh, with its user-friendly aspect, graphical-user interface, overlapping windows, and mouse was inspired by a 1979 visit Steve Jobs and a group of engineers paid to XEROX PARC, located in the Stanford Research Park. In other words, Apple was the product of its Silicon Valley environment and technological roots.

Culture

This brings us to the second force behind the birth of Silicon Valley: culture. When Shockley, his transistor and his recruits arrived in 1955, the valley was still largely agricultural, and the small local industry had a distinctly high-tech (or as they would have said then, “space age”) focus. The largest employer was defense contractor Lockheed. IBM was about to open a small research facility. Hewlett-Packard, one of the few homegrown tech companies in Silicon Valley before the 1950s, was more than a decade old.

Stanford, meanwhile, was actively trying to build up its physics and engineering departments. Professor (and Provost from 1955 to 1965) Frederick Terman worried about a “brain drain” of Stanford graduates to the East Coast, where jobs were plentiful. So he worked with President J.E. Wallace Sterling to create what Terman called “a community of technical scholars” in which the links between industry and academia were fluid. This meant that as the new transistor-cum-microchip companies began to grow, technically knowledgeable engineers were already there.

Woz and Jobs. Photo courtesy Computer History Museum.

These trends only accelerated as the population exploded. Between 1950 and 1970, the population of Santa Clara County tripled, from roughly 300,000 residents to more than 1 million. It was as if a new person moved into Santa Clara County every 15 minutes for 20 years. The newcomers were, overall, younger and better educated than the people already in the area. The Valley changed from a community of aging farmers with high school diplomas to one filled with 20-something PhDs.

All these new people pouring into what had been an agricultural region meant that it was possible to create a business environment around the needs of new companies coming up, rather than adapting an existing business culture to accommodate the new industries. In what would become a self-perpetuating cycle, everything from specialized law firms, recruiting operations and prototyping facilities; to liberal stock option plans; to zoning laws; to community college course offerings developed to support a tech-based business infrastructure.

Historian Richard White says that the modern American West was “born modern” because the population followed, rather than preceded, connections to national and international markets. Silicon Valley was bornpost-modern, with those connections not only in place but so taken for granted that people were comfortable experimenting with new types of business structures and approaches strikingly different from the traditional East Coast business practices with roots nearly two centuries old.

From the beginning, Silicon Valley entrepreneurs saw themselves in direct opposition to their East Coast counterparts. The westerners saw themselves as cowboys and pioneers, working on a “new frontier” where people dared greatly and failure was not shameful but just the quickest way to learn a hard lesson. In the 1970s, with the influence of the counterculture’s epicenter at the corner of Haight and Ashbury, only an easy drive up the freeway, Silicon Valley companies also became famous for their laid-back, dressed-down culture, and for their products, such as video games and personal computers, that brought advanced technology to “the rest of us.”

Money

The third key component driving the birth of Silicon Valley, along with the right technology seed falling into a particularly rich and receptive cultural soil, was money. Again, timing was crucial. Silicon Valley was kick-started by federal dollars. Whether it was the Department of Defense buying 100% of the earliest microchips, Hewlett-Packard and Lockheed selling products to military customers, or federal research money pouring into Stanford, Silicon Valley was the beneficiary of Cold War fears that translated to the Department of Defense being willing to spend almost anything on advanced electronics and electronic systems. The government, in effect, served as the Valley’s first venture capitalist.

The first significant wave of venture capital firms hit Silicon Valley in the 1970s. Both Sequoia Capital and Kleiner Perkins Caufield and Byers were founded by Fairchild alumni in 1972. Between them, these venture firms would go on to fund Amazon, Apple, Cisco, Dropbox, Electronic Arts, Facebook, Genentech, Google, Instagram, Intuit, and LinkedIn — and that is just the first half of the alphabet.

This model of one generation succeeding and then turning around to offer the next generation of entrepreneurs financial support and managerial expertise is one of the most important and under-recognized secrets to Silicon Valley’s ongoing success. Robert Noyce called it “re-stocking the stream I fished from.” Steve Jobs, in his remarkable 2005 commencement address at Stanford, used the analogy of a baton being passed from one runner to another in an ongoing relay across time.

So that’s how Silicon Valley emerged. Why it has it endured?

After all, if modern Silicon Valley was born in the 1950s, the region is now in its seventh decade. For roughly two-thirds of that time, Valley watchers have predicted its imminent demise, usually with an allusion to Detroit. First, the oil shocks and energy crises of the 1970s were going to shut down the fabs (specialized factories) that build microchips. In the 1980s, Japanese competition was the concern. The bursting of the dot-com bubble, the rise of formidable tech regions in other parts of the world, the Internet and mobile technologies that make it possible to work from anywhere: all have been heard as Silicon Valley’s death knell.

The Valley of Heart’s Delight, pre-technology. OSU Special Collections.

The Valley economy is notorious for its cyclicity, but it has indeed endured. Here we are in 2015, a year in which more patents, more IPOs, and a larger share of venture capital and angel investments have come from the Valley than ever before. As arecent report from Joint Venture Silicon Valley put it, “We’ve extended a four-year streak of job growth, we are among the highest income regions in the country, and we have the biggest share of the nation’s high-growth, high-wage sectors.” Would-be entrepreneurs continue to move to the Valley from all over the world. Even companies that are not started in Silicon Valley move there (witness Facebook).

Why? What is behind Silicon Valley’s staying power? The answer is that many of the factors that launched Silicon Valley in the 1950s continue to underpin its strength today even as the Valley economy has proven quite adaptable.

Technology

The Valley still glides in the long wake of the transistor, both in terms of technology and in terms of the infrastructure to support companies that rely on semiconductor technology. Remember the pearl. At the same time, when new industries not related directly to semiconductors have sprung up in the Valley — industries like biotechnology — they have taken advantage of the infrastructure and support structure already in place.

Money

Venture capital has remained the dominant source of funding for young companies in Silicon Valley. In 2014, some $14.5 billion in venture capital was invested in the Valley, accounting for 43 percent of all venture capital investments in the country. More than half of Silicon Valley venture capital went to software investments, and the rise of software, too, helps to explain the recent migration of many tech companies to San Francisco. (San Francisco, it should be noted, accounted for nearly half of the $14.5 billion figure.) Building microchips or computers or specialized production equipment — things that used to happen in Silicon Valley — requires many people, huge fabrication operations and access to specialized chemicals and treatment facilities, often on large swaths of land. Building software requires none of these things; in fact, software engineers need little more than a computer and some server space in the cloud to do their jobs. It is thus easy for software companies to locate in cities like San Francisco, where many young techies want to live.

Culture

The Valley continues to be a magnet for young, educated people. The flood of intranational immigrants to Silicon Valley from other parts of the country in the second half of the twentieth century has become, in the twenty-first century, a flood of international immigrants from all over the world. It is impossible to overstate the importance of immigrants to the region and to the modern tech industry. Nearly 37 percent of the people in Silicon Valley today were born outside of the United States — of these, more than 60 percent were born in Asia and 20 percent in Mexico. Half of Silicon Valley households speak a language other than English in the home. Sixty-five percent of the people with Bachelors degrees working in the valley were born in another country. Let me say that again: 2/3 of people in the Valley who have completed their college education are foreign born.

Here’s another way to look at it: From 1995 to 2005, more than half of all Silicon Valley startups had at least one founder who was born outside the United States.[13] Their businesses — companies like Google and eBay — have created American jobs and billions of dollars in American market capitalization.

Silicon Valley, now, as in the past, is built and sustained by immigrants.

Gordon Moore and Robert Noyce at Intel in 1970. Photo courtesy Intel.

Stanford also remains at the center of the action. By one estimate, from 2012, companies formed by Stanford entrepreneurs generate world revenues of $2.7 trillion annually and have created 5.4 million jobs since the 1930s. This figure includes companies whose primary business is not tech: companies like Nike, Gap, and Trader Joe’s. But even if you just look at Silicon Valley companies that came out of Stanford, the list is impressive, including Cisco, Google, HP, IDEO, Instagram, MIPS, Netscape, NVIDIA, Silicon Graphics, Snapchat, Sun, Varian, VMware, and Yahoo. Indeed, some critics have complained that Stanford has become overly focused on student entrepreneurship in recent years — an allegation that I disagree with but is neatly encapsulated in a 2012 New Yorker article that called the university“Get Rich U.”

Change

The above represent important continuities, but change has also been vital to the region’s longevity. Silicon Valley has been re-inventing itself for decades, a trend that is evident with a quick look at the emerging or leading technologies in the area:

• 1940s: instrumentation

• 1950s/60s: microchips

• 1970s: biotech, consumer electronics using chips (PC, video game, etc)

• 1980s: software, networking

• 1990s: web, search

• 2000s: cloud, mobile, social networking

The overriding sense of what it means to be in Silicon Valley — the lionization of risk-taking, the David-versus-Goliath stories, the persistent belief that failure teaches important business lessons even when the data show otherwise — has not changed, but over the past few years, a new trope has appeared alongside the Western metaphors of Gold Rushes and Wild Wests: Disruption.

“Disruption” is the notion, roughly based on ideas first proposed by Joseph Schumpeter in 1942, that a little company can come in and — usually with technology — completely remake an industry that seemed established and largely impervious to change. So: Uber is disrupting the taxi industry. Airbnb is disrupting the hotel industry. The disruption story is, in its essentials, the same as the Western tale: a new approach comes out of nowhere to change the establishment world for the better. You can hear the same themes of adventure, anti-establishment thinking, opportunity and risk-taking. It’s the same song, with different lyrics.

The shift to the new language may reflect the key role that immigrants play in today’s Silicon Valley. Many educated, working adults in the region arrived with no cultural background that promoted cowboys or pioneers. These immigrants did not even travel west to get to Silicon Valley. They came east, or north. It will be interesting to see how long the Western metaphor survives this cultural shift. I’m betting that it’s on its way out.

Something else new has been happening in Silicon Valley culture in the past decade. The anti-establishment little guys have become the establishment big guys. Apple settled an anti-trust case. You are hearing about Silicon Valley companies like Facebook or Google collecting massive amounts of data on American citizens, some of which has ended up in the hands of the NSA. What happens when Silicon Valley companies start looking like the Big Brother from the famous 1984 Apple Macintosh commercial?

A Brief Feint at the Future

I opened these musings by defining Silicon Valley as a physical location. I’m often asked how or whether place will continue to matter in the age of mobile technologies, the Internet and connections that will only get faster. In other words, is region an outdated concept?

I believe that physical location will continue to be relevant when it comes to technological innovation. Proximity matters. Creativity cannot be scheduled for the particular half-hour block of time that everyone has free to teleconference. Important work can be done remotely, but the kinds of conversations that lead to real breakthroughs often happen serendipitously. People run into each other down the hall, or in a coffee shop, or at a religious service, or at the gym, or on the sidelines of a kid’s soccer game.

It is precisely because place will continue to matter that the biggest threats to Silicon Valley’s future have local and national parameters. Silicon Valley’s innovation economy depends on its being able to attract the brightest minds in the world; they act as a constant innovation “refresh” button. If Silicon Valley loses its allure for those people — if the quality of public schools declines so that their children cannot receive good educations, if housing prices remain so astronomical that fewer than half of first-time buyers can afford the median-priced home, or if immigration policy makes it difficult for high-skilled immigrants who want to stay here to do so — the Valley’s status, and that of the United States economy, will be threatened. Also worrisome: ever-expanding gaps between the highest and lowest earners in Silicon Valley; stagnant wages for low- and middle-skilled workers; and the persistent reality that as a group, men in Silicon Valley earn more than women at the same level of educational attainment. Moreover, today in Silicon Valley, the lowest-earning racial/ethnic group earns 70 percent less than the highest earning group, according to the Joint Venture report. The stark reality, with apologies to George Orwell, is that even in the Valley’s vaunted egalitarian culture, some people are more equal than others.

Another threat is the continuing decline in federal support for basic research. Venture capital is important for developing products into companies, but the federal government still funds the great majority of basic research in this country. Silicon Valley is highly dependent on that basic research — “No Basic Research, No iPhone” is my favorite title from a recently released report on research and development in the United States. Today, the US occupies tenth place among OECD nations in overall R&D investment. That is investment as a percentage of GDP — somewhere between 2.5 and 3 percent. This represents a 13 percent drop below where we were ten years ago (again as a percentage of GDP). China is projected to outspend the United States in R&D within the next ten years, both in absolute terms and as a fraction of economic development.

People around the world have tried to reproduce Silicon Valley. No one has succeeded.

And no one will succeed because no place else — including Silicon Valley itself in its 2015 incarnation — could ever reproduce the unique concoction of academic research, technology, countercultural ideals and a California-specific type of Gold Rush reputation that attracts people with a high tolerance for risk and very little to lose. Partially through the passage of time, partially through deliberate effort by some entrepreneurs who tried to “give back” and others who tried to make a buck, this culture has become self-perpetuating.

The drive to build another Silicon Valley may be doomed to fail, but that is not necessarily bad news for regional planners elsewhere. The high-tech economy is not a zero-sum game. The twenty-first century global technology economy is large and complex enough for multiple regions to thrive for decades to come — including Silicon Valley, if the threats it faces are taken seriously.